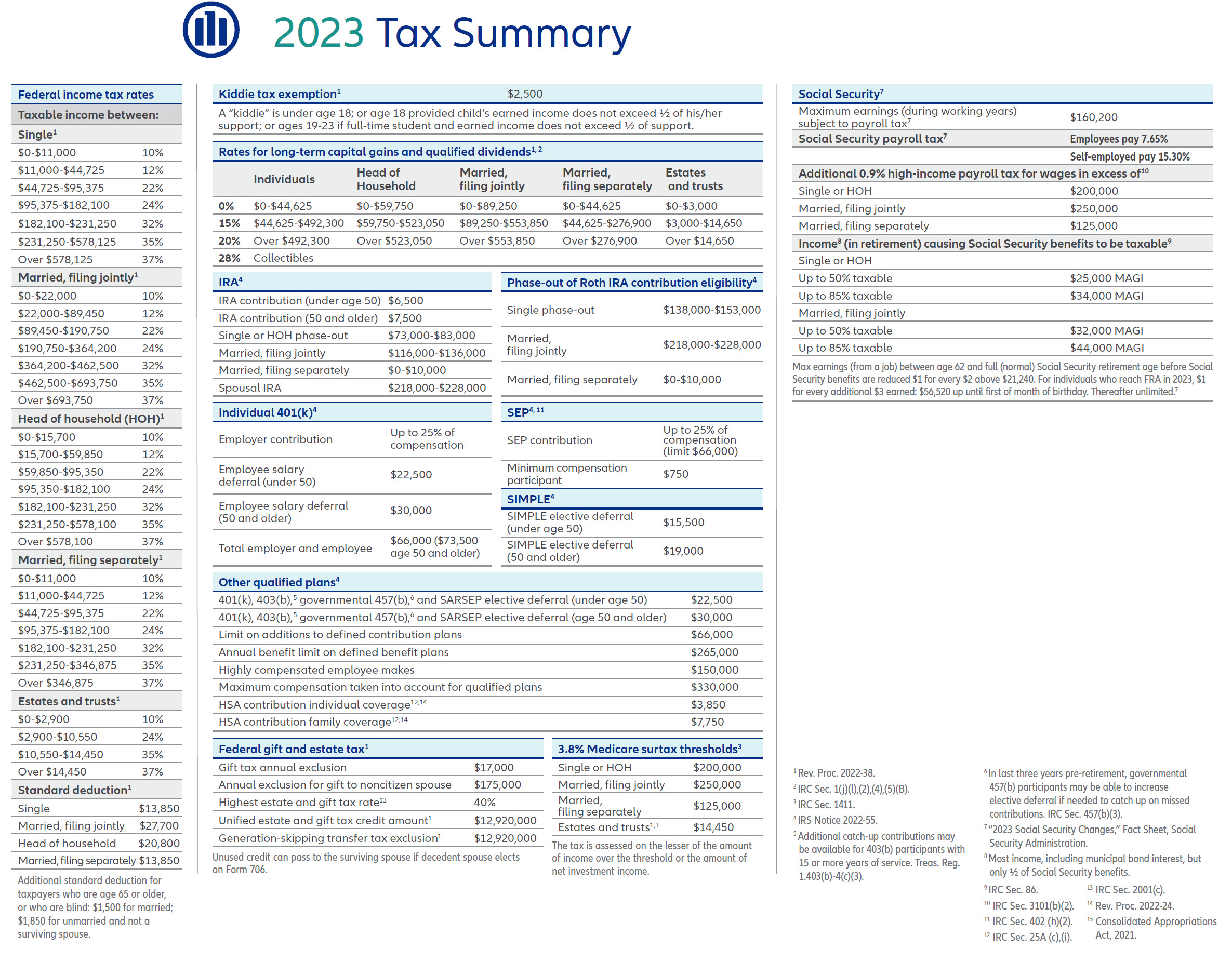

How much will you pay in federal income taxes in 2023?

As an investor, you should always be aware of the tax implications of your financial decisions. Planning your taxes is essential. The IRS has released the tax rates and essential tax facts for investors for 2023 . These rates will apply to your income earned in 2023 and filed in 2024. Depending on your filing status and income level, you may fall into one of seven tax brackets, ranging from 10% to 37%. You may also qualify for a standard and additional deduction if you are 65 or older or blind. In addition, you should be aware of the tax rules for long-term capital gains, qualified dividends, IRAs, Roth IRAs, and kiddie taxes.

This table can help you plan your investment strategy for the next year and optimize your tax savings. For example, depending on your income bracket, you can see how much tax you will pay on your capital gains and dividends. You can also see how much you can contribute to your IRA or Roth IRA and how much you can deduct from your taxable income. You can also see how much of your child’s unearned income will be subject to the kiddie tax. Knowing your marginal tax bracket and understanding tax rules can help you make informed investment decisions and avoid tax return surprises.

Consider Converting to a Roth IRA for Tax-Free Growth

Investors who expect to move into a higher tax bracket in the future may want to consider converting traditional IRA balances to Roth IRAs now. A Roth conversion allows you to pay income taxes now on the amount converted in exchange for tax-free growth and withdrawals later. This can provide significant savings down the road.

When evaluating a conversion, be aware it will increase your taxable income for that year, which could push you into a higher bracket. Run the numbers to see if it still makes sense. While income limits on Roth conversions have been eliminated, you cannot undo a conversion after the tax filing deadline. For many investors, a Roth conversion can be a strategic move to create tax-free income in retirement.

Fun Facts about Qualified Dividend Income and Long-term Capital Gains

Did you know that a married couple can earn up to $117,000 from qualified dividends and long-term capital gains and owe zero US income taxes for tax year 2023, assuming the couple has no other income? For high earners, the marginal tax rate on QDI and LTCG is capped at 20% plus 3.8% for the Medicare surtax. That is nearly 50% lower than the top marginal tax rate on ordinary income.

The Benefits of Mixing Qualified and Nonqualified Withdrawals

Some investors may believe they should spend down their nonqualified accounts, such as taxable brokerage accounts before accessing their qualified accounts, such as IRAs or 401(k)s. However, this approach may not be ideal for tax purposes. The reason is that your tax bracket matters. As you withdraw more funds from your qualified accounts, your taxable income increases, which may push you into a higher marginal tax bracket. This means you will pay a higher percentage of your income in taxes.

However, if you take out some income from your nonqualified accounts or Roth IRA, you may be able to keep your taxable income lower and stay in a lower tax bracket. This can help you save money on taxes in the long run, as your income and tax brackets change in the future.

Of course, this approach depends on your situation and goals. You should consult with a tax professional before making any decisions. But in general, you should not overlook the effect of future tax brackets when planning your withdrawals. By diversifying your income sources, you can optimize your tax savings and enjoy your retirement.